Labour Market, 2013

More locals employed in 2013, While Foreign Growth Slowed

14 March 2014

Key Findings from the Labour Market, 2013

- Unemployment remained low amid the tight labour market, while employment creation remained high, mainly driven by locals. The annual average citizen unemployment rate in 2013 was 2.9%. Local employment rose more quickly (4.0%) than in 2012 (2.9%), while foreign employment gains continued to moderate (2013: 4.2%; 2012: 5.9%) amid the foreign manpower tightening measures.

- Real income growth strengthened, driven by the tight labour market and lower inflation. The growth in real median monthly income (including employer CPF contributions) for full-time employed Singapore citizens was 4.6% in 2013, up from 1.2% in 2012.

MOM’s Statement on Labour Market Developments

- MOM also released its Statement on Labour Market Developments, which conveys the Ministry’s outlook for 2014. The key thrusts of the Statement are:

• Tight Labour Market in 2014 - The Singapore labour market is expected to tighten further this year as previously announced foreign workforce policy measures come into effect. This will place upward pressure on wages. Unemployment is likely to remain low, while local employment should continue to register gains in 2014.

• Firms must continue to improve productivity and reduce reliance on manpower - The current high rate of local workforce growth will be difficult to sustain in the long run due to demographic constraints. Labour productivity growth has also lagged behind income growth slightly in the past five years. Firms will need to implement more manpower-lean methods of driving business growth in order to survive and thrive.

• MOM will monitor the impact of previously announced foreign worker policy measures on employment, productivity, and incomes, and continue to take progressive steps to moderate foreign workforce growth to more sustainable levels.

- The Labour Market, 2013 report is available on the MOM's Statistics and Publications webpage.

Ministry of Manpower Statement on Labour Market Developments

14 March 2014

Introduction

- In 2013, the Ministry of Manpower (MOM) continued its approach of taking progressive steps to raise the quality of the foreign workforce and moderate foreign employment growth. This is part of the Government’s effort to achieve quality economic growth driven by sustained productivity improvement. MOM takes into account the rate of employment growth, productivity growth, and the real income growth of Singaporeans when calibrating its manpower policy measures.

- Total employment growth was strong in 2013, driven in large part by local1 employment growth, while foreign employment growth moderated. Labour market conditions continued to be tight, with the seasonally-adjusted citizen unemployment rate remaining low at 2.8% in December 2013. Real median incomes2 for full-time employed citizens grew by 4.6% in 2013, while overall labour productivity growth was flat.

Review of 2013

Employment

Unemployment rate remained low

- The unemployment rate remained low amid the tight labour market. The seasonally-adjusted citizen unemployment rate was low at 2.8% in December 2013, slightly lower than the 2.9% in December 2012.

Total employment growth remained high in 2013

-

Total employment (excluding FDWs3) growth remained high in 2013 at 4.2% (or 131,300) in 2013, similar to the increase of 4.2% (or 125,800) in 2012. The increase in total employment in 2013 was driven mainly by a strong increase in local employment.

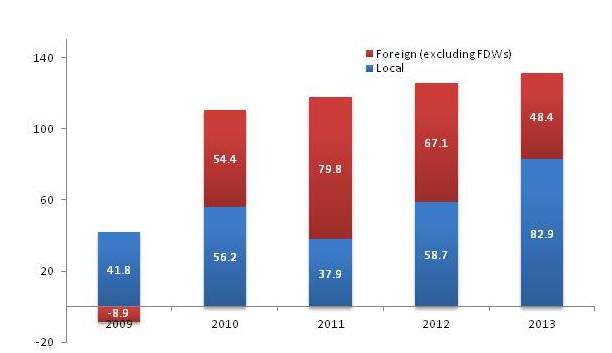

Figure 1: Employment Change (excluding FDWs) 2009 – 2013

Local employment growth was higher in 2013 than 2012

Local employment growth was higher in 2013 than 2012

- Local employment growth was stronger at 4.0% (82,900) in 2013, compared to 2.9% (58,700) in 2012, as firms tried harder to bring economically inactive residents back into employment amidst curbs on foreign employment growth. This was reflected in the increase in employment rates of older residents and female residents.4 Overall, the bulk of the growth in local employment were in the Services sector (77,100), led by the Community, Social & Personal Services, Professional Services, Admin & Support Services and Food & Beverage Services industries.

Foreign employment growth continued to slow

- Growth in foreign employment (excluding FDWs) slowed for the second consecutive year to 4.6% (48,400) in 2013, down from 6.8% (67,100) in 2012, as previously announced foreign manpower tightening measures started to take effect. These included the reduction in Dependency Ratio for the Services sector5 and increased levy rates across all sectors. The bulk of foreign manpower growth came from the Construction sector (31,600), due to infrastructure projects such as the Downtown and Thomson MRT lines. Excluding Construction and FDWs, foreign employment grew by 2.3% (16,800) in 2013, down from 4.6% (32,200) in 2012.

- By pass-type, the number of Employment Pass holders grew by 1,300 in 2013 after contracting by 1,600 in 2012. S-pass holder growth moderated to 18,500 in 2013, from 28,500 in 2012. Work Permit holder (excluding FDWs) growth slowed to 28,600 in 2013, from 40,300 in 2012. (See Annex A for more details)

- In 2013, foreign workers comprised 36.9% of total employment growth (excluding FDWs), down from 53.3% in 2012. Overall, the foreign share of total employment (excluding FDWs) reached 33.8% in end 2013.

Layoffs increased slightly but re-entry into employment improved

- As economic restructuring efforts continued, 11,560 workers were laid off in 2013, slightly higher than 11,010 in 20126 . The increase in layoffs stemmed mainly from Electronics and the Construction sector. Nevertheless, the rate of re-entry into employment within 6 months improved for the third successive quarter to reach 59% in December 2013. Overall, the labour market remained tight, with the ratio of job vacancies to jobseekers increasing to 1.44 in December 2013, from 1.05 in December 2012.

Productivity

Productivity growth improved in the second half of the year

- Following several quarters of negative or flat growth, labour productivity rose over the year by 1.6% and 1.4% respectively in the third and fourth quarters of 2013. This was mainly driven by improvements in the Manufacturing sector and Wholesale & Retail Trade industry, as well as the continued productivity growth in the Finance & Insurance industry. However, Construction and the remaining Service industries continued to see flat or negative productivity growth. Taking into account the poorer productivity growth in the first half of 2013, overall labour productivity growth was flat in 2013, an improvement from 2012 when labour productivity declined by 2.0%. Over a five year period from 2008 to 2013, labour productivity growth was 1.5% per annum.

Income

Incomes increased for Singaporeans

- The real median monthly income (including employer CPF contributions) of full-time employed citizens increased by 4.6% in 20137. This reflected strong nominal income gains amidst tight labour market conditions, as well as moderating inflation8. Over a five year period from 2008 to 2013, real median income increased by 1.7% per annum, while real income at the 20th percentile (P20) grew faster at 2.0% per annum. This has led to a narrowing of the gap between median and P20 incomes.

2014 Labour Market Outlook

- In February 2014, the Ministry of Trade and Industry announced that the Singapore economy is expected to grow by 2 - 4% in 2014. MOM expects labour demand to remain strong in 2014, barring severe unexpected shocks in the external economy.

- The Construction sector is expected to see strong labour demand on account of ongoing infrastructure development. These include the construction of the Downtown and Thomson MRT lines, hospitals and nursing homes, as well as public and private sector housing projects. Labour demand in the Manufacturing sector is expected to come mainly from the Marine and General Manufacturing industries.

- Labour demand in the Services sector is also expected to be strong. In particular, labour demand from the Retail Trade, Accommodation and Food & Beverage Services industries will be driven by the opening of several hotels and shopping malls in 2014. As previously announced foreign workforce tightening measures for the Services sector (such as the reduction of DRC for renewal applications from 50% to 45% and increases in foreign worker levies) come into force in July 2014, labour market conditions for these industries will tighten further, especially for firms that rely on more manpower-intensive and less productive models of operation.

- Overall, the Singapore labour market is expected to remain tight in 2014. This will place upward pressure on incomes. While some increase in redundancies is expected as part of economic restructuring, unemployment is likely to remain low as job creation will be strong. With increasingly binding foreign manpower constraints, local employment should continue to register gains in 2014.

Conclusion

- While incomes have grown at a healthy rate in the past five years, labour productivity growth has lagged slightly. There is a need to sustain and broaden the recent improvement in productivity growth, especially in the Construction sector and the more labour-intensive industries within the Services sector.

- Firms have increasingly turned to hiring more local workers to meet their manpower needs as foreign workforce policies are tightened. However, the current rate of local employment growth will be difficult to sustain in the long run, due to demographic constraints. Firms will need to implement more manpower-lean methods of driving business growth in order to survive and thrive. MOM is reviewing the CET Masterplan to support the re-skilling and upgrading of our workforce to meet the needs of our economy.

- The Ministry of Manpower will monitor the impact of previously announced foreign workforce policy measures on employment, productivity, and incomes, and continue to take progressive steps to moderate foreign workforce growth to more sustainable levels.

1 Refers to Singapore Citizens and Permanent Residents.

2 Real median gross monthly income (including Employer CPF contributions), deflated by Consumer Price Index (CPI) for all items.

3 Foreign Domestic Workers.

4 The employment rates for older residents aged 55 to 64 and women in the prime-working ages of 25 to 54 rose to new highs of 65.0% and 74.3% in June 2013, from 64.0% and 74.0%, respectively in June 2012.

5 The Dependency Ratio Ceiling (DRC) for Services companies was reduced from 45% to 40%, for all new applications, with effect from 1 July 2013.

6 Data pertain to private sector establishments (each with at least 25 employees) and the public sector.

7 When adjusted using CPI All-items less imputed rentals on owner-occupied accommodation (which have no impact on the cash expenditure of households who are owner-occupiers), real median income growth was 5.2% in 2013.

8 The CPI All-items rose by 2.4% (1.9%) in 2013, compared to 4.6% (3.6%) in 2012. Figures in parenthesis refer to change in CPI All-items less imputed rentals on owner-occupied accommodation.